Rod Bailey, Landscape Industry Certified, is a management consultant based in Woodinville, WA. Having worked with all types of landscape contractors for several years, Bailey says many simply do not understand their financial reports.

"Most contractors seem to be using QuickBooks' standard formats and regard their financial reports as an interesting historical track record," Bailey says. "They have not learned that their financials are, and should be, the basis for looking into the future more than the past, and are critical planning, guiding and managing tools."

Bailey adds that he's talking about the two most important reports: The Balance Sheet and the Income Statement, often called the Profit & Loss Report. Let’s take a quick look at the formats that should be used for each.

Report #1: The Balance Sheet

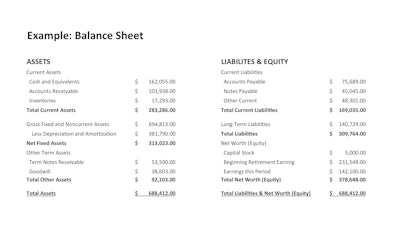

The Balance Sheet is linked to a point in time, such as the end of a fiscal year, quarter, or month. It is like a snapshot that shows how things were at that moment. It is a picture of what you own (Assets), what you owe (Liabilities) and what’s left over (Equity, or Owner’s Net Worth). It is typically formatted as you'll see in the illustration, Example: Balance Sheet.

One reason this report is called the “Balance Sheet” is because it must always be in balance with Total Liabilities & Equity equal to Total Assets. The Balance Sheet equation is Assets minus Liabilities equals Equity.

Read next: Finance for Landscaping Business Owners of all Sizes

Report #2: The Income Statement (Profit & Loss Report)

The Income Statement, or Profit & Loss Report, covers a period of time or series of time periods, such as months, quarters or years. If the Balance Sheet is like a snapshot, the P&L might be likened to a movie.

The P&L says: Here’s how much money we earned, how much money it cost, and how much money is left over for Profit. The P&L's basic equation is Revenue (Sales) minus Expenses equals Profit (or Loss).

There should be five major sections to a P&L:

- Revenue (Sales)

- Direct Costs

- Indirect Expense (one component of overhead)

- General & Administrative (G&A) Expense (second component of overhead)

- Net Profit

For an example of what a typical Profit & Loss Report looks like, see illustration, Example: Income Statement/P&L Report.

Certainly each section of the P&L includes the details by type of revenue and expense, Bailey points out. You should also, as shown, have a column to determine the percentage relationship to total sales for comparison to your own history or to other companies in your industry. (NOTE: For those who would like a more detailed “Chart of Accounts”, you can contact Bailey via the email address shown at the end of this article.)

"One of the problems I often encounter is a format where Cost of Sales usually includes everything but the kitchen sink, as is typical on tax returns," Bailey points out.

As shown in the illustration, Direct Costs include only those costs you can track directly to each job you do. They are the items you include on your estimating sheet when you are bidding a job.

"Indirect Expenses are those you can’t track to each job, but you can track to each department, service or product line you are producing," Bailey says. "Computation of the Gross Margin and Contribution Margin are two of the most important numbers you need to determine for planning, measuring and managing your business."

One additional misunderstanding Bailey says he frequently sees is the treatment of Wages and Salaries under a single account titled Labor Expense. All labor, salaries and commissions should be recorded and tracked separately by type. Direct Labor is tracked in the Direct Cost section, which may include some allocation of Managers' or Owners' Salaries if, in fact, that person(s) works as “hands on” in the field directly on jobs.

Indirect Labor should be tracked and reported in the Indirect Expense Section. It is usually mechanic, supervisory and management as well as the indirect hours paid to direct labor employees for time not chargeable to the jobs such as shop time, training time, vacation, holidays, and in some companies, travel.

Read next: Six Invaluable Financial Reports to Help You Lead Your Company

Making sense of these two reports

So how do we use all of this information for planning and managing? Bailey says you start by making some important calculations that show the relationships made evident in your financial statements. Then you use these ratios to compare yourself over time, and to compare yourself to others in your industry.

Some of these calculations and ratios are from the Balance Sheet, some from the Profit & Loss, and some from inter-statement relationships. Here's a look at 10 of the most valuable, using data from our two illustrations to provide examples.

Balance Sheet Ratios

Current Ratio = Current Assets / Current Liabilities

Example: $283,286 / $169,035 = 1.68

Bailey says anything over 1.0 is good. But if you're below that, "You better be in the maintenance business and have very reliable and predictable cash flow," Bailey points out. "This ratio is regarded as a measure of your ability to pay your bills and stay current."

Debt to Equity = Total Liabilities / Total Net Worth (Equity)

Example: $309,764 / $378,648 = 0.82

Bailey says your banker is going to want to know that you have as much skin in the game as they do. Your ratio ideally should be under 1, and definitely not over 2.

Asset Newness = Net Fixed Assets / Gross Fixed and Noncurrent Assets

Example: $313,023 / $694,813 = 0.45

Bailey says this ratio should be in the range of 0.4 to 0.6. "If it's too high, you might be spending too much on new equipment," he adds. "If it's too low, you might be looking at a bunch of tired out junk that you will have to replace within the next few years (depending on the method of depreciation you're using)."

Profit & Loss Ratios (as percent of sales)

Gross Profit Margin = Total Revenue (Sales) - Total Direct Costs

Example: 100% - 49% = 51%

Bailey says this is usually in the 45-55% range for most landscape companies. For maintenance-heavy companies, it's often 50-55% since they aren't using as much material. For design/build companies, on the other hand, it's often 45-50%. "If your gross profit margin is falling below these targets, you may be operating inefficiently or underpricing your work," Bailey points out.

Contribution Margin = Gross Margin - Total Indirect Expense

Example: 51% - 24% = 27%

Bailey says a good goal to shoot for is 22-32%. If your contribution margin is lower than that, it might indicate inefficient operations. Additionally, if your gross profit margin is landing in that ideal 45-55% range but your contribution margin is still falling short, you need to seriously look at your indirect expenses and identify where you might be going wrong. Perhaps you are spending too much on equipment repairs and tools/supplies, for instance.

Net Profit = Contribution Margin - G&A Expense

Example: 27.4% - 16.5% = 10.9%

"Net profit is that proverbial 'bottom line,'" Bailey explains. "A good goal is 5-12%. If you are significantly outside this range, you should understand why. There may be valid reasons, particularly if you are a highly leveraged company with a high Debt to Equity ratio in a high-interest market."

Inter-Statement Ratios

Return on Assets = Net Profit / Total Assets

Example: $142,100 / $688,412 = 20.6%

"This is typically referred to as an ROA," he adds. "It's a measure of how effectively you are using your total invested capital plus debt. As a contractor, you are a gambler and should expect a high return relative to other more secure investments. A good goal is 15-22%."

Return on Equity = Net Profit / Total Net Worth (Equity)

Example: $142,100 / $378,648 = 37.5%

This should land in the 25-35% range. "This is typically called an ROI," Bailey says. "It's a measure of the return earned on the money you and/or other investors have put into the business. It's a very important number. If it's not up toward the 30% range, maybe you should just sell your business and put your money into safer investments."

Asset Turnover = Total Sales / Total Assets

Example: $1,300,000 / $688,412 = 1.9

A good goal is 2.5 to 5.0. "This is a measure of how effectively you use your assets to generate sales," Bailey explains. "A low number like this one (1.9) may indicate that you've invested more in equipment and facility than you really need, or perhaps that you're simply not using your equipment and facility effectively. You may have too much idle capacity."

Average Collection Days = Accounts Receivable / (Sales / Days in Period)

Example: $103,938 / ($1,300,000 / 365) = $103,938 / 3,561 = 29.18 days

Bailey says a good target is 25-45 days. "If you sell on 30-day credit terms, this number should be under 30 days," he explains. "If the number is high, look at your Current Ratio and compare Receivables to Payables. Typically, installation and bid/build contractors show over 45 days, and should examine their credit terms and collection efforts."

In conclusion

"These are just a few of the many ratios you can compute and analyze," Bailey reminds. "I regard these as 10 of the most critical. A fuller discussion of ratios, costs and operating data can be found in PLANET’s Operating Cost Study for the Green Industry, updated and published every three to five years. Other comparative data and ratios are periodically issued by many consultants working with the industry based on their own client experiences.

"You should compute and track your ratios at least annually, and preferably most of them on a quarterly basis," Bailey continues. "Watch for trends in your ratios that may be significant, and use your own experience when you are doing your short- and long-range planning and budgeting. You should also compare your experience to the PLANET Operating Cost Study.

"I have included a number of loose guideline ranges that I regard as significant in my computations in this article. You are your own best standard and should check the trends in your data. I do not regard it as essential that you fall within the guideline ranges I have established. But if you don't, I urge you to understand why. The ranges I have shown represent median experience of contractors in the industry. You may set your targets well ahead of these medians on the belief that through intelligent management you should be able to beat the medians. You are right! If you have any questions please contact me.

*This article was originally published in 2014.